Table Of Content

| S.No. | Particular |

| 1 | What makes a good portfolio |

| 2 | What are the risks in the market |

| 3 | The need to hedge your portfolio |

| 4 | How to hedge against unsystematic risk |

| 5 | How to hedge against systematic risk |

| 6 | Hedging using Single Stock Futures |

| 7 | Hedging using Index Futures |

| 8 | Conclusion |

What Makes A Good Portfolio?

A good portfolio generally comprises two basic things:

- Having low risk

- Having high returns

Generally, we assume investors are risk-averse and do not want to take risks. Let us say that Harish is a passive investor. Harish invests in a 10-year government security and receives around a 7% interest rate. This is a risk-free rate since the Government of India will always pay the interest and will not default. If any case arises, GOI could always print more money.

Suppose the CPI (Consumer Price Index) inflation is currently at 5%. Hence, the real interest rate that Harish is getting is around 2%. Harish is a passive investor because he does not try to beat any benchmark index. Harish is also a very risk-averse investor. He will not invest in riskier assets if the return is not significantly high. His risk currently is zero.

Now, Harish is presented with an opportunity to invest in the equity market. Equity markets contain risks with them. If he invests in 5 stocks with a total risk of 5%, then he would want a return greater than 5%. This is a risk-averse investor, who wants more than a unit percentage increase in return for a unit percentage in risk.

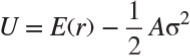

CFA institute defines a formula for the utility of the investor:

Where U is the utility

E(r) is the expected return from the portfolio

is the variance of the portfolio (risk) and

A is the coefficient of risk aversion. (The higher the A, the more risk-averse the investor)

Hence, for a higher risk-averse investor, a given portfolio might provide the same utility as an investor, which is less risk-averse. To get the same utility, either the risk (variance) should be lower or E(r) should be higher.

Let us now come back to Harish, there could be different combinations of risk and return, which will give him the same utility. This can be shown in a risk-return curve. {Mean – Variance graph}

This curve is called an indifference curve as Harish is indifferent to any possible combination of risk and return, till it lies on that curve. With an increase in risk from P to Q, the return increased from P to Q is greater. Hence, it is not a straight line but a curve.

The possible combinations of risk & return on this indifference curve lead to the same utility since its ‘A’ is fixed.

By having the same 5 equities in his portfolio, Harish can have different sets of risks and returns by varying the capital allocation in each of those 5 equities to find the optimal mix for himself.

If in this portfolio, Harish also allocated funds to the G-Secs he already had, then the overall portfolio risk and return would come down. Hence, if Harish is not satisfied with the risk-return from the equities, he can always choose a different asset to invest in and reduce his risk-return profile to fit his needs.

Therefore, we can conclude this part by stating that for a good portfolio, one needs a low-risk and a high-return portfolio and that could be done by :

- Choosing the right assets to invest in (A mixture of Equity, Commodity, and Fixed Income Securities )

- Optimizing capital allocation in those particular

Risks In The Market

Different securities have different risks that come with them. If Harish invests in a corporate bond, then he takes on the credit risk. The virtue of bonds is that they give out coupons every year or six months. But, there is always a risk that the company might default on these coupons or the company can shut down. This is called the credit risk. The credit risk is managed by giving ratings to companies. Hence, a company with a AAA rating is less likely to default compared to a company with a rating of C.

In equity markets, we have mainly 2 types of risks:

- Systematic Risks: Systematic risk refers to the portion of total risk that arises from external factors outside the control of any specific company or individual. This type of risk affects all investments or securities, making it unavoidable and non-diversifiable.

- Unsystematic Risks: Unsystematic risk, also referred to as non-systematic risk, specific risk, diversifiable risk, or residual risk, pertains to the risk associated with a particular company or industry. In an investment portfolio, this type of risk can be mitigated by diversifying.

The total risk in the market for a portfolio hence comprises of Systematic and Unsystematic risk. It comprises both the risk that is because of the company or industry and the risk that is because of the virtue of it being listed. Some risks can be easily eliminated while we cannot eliminate some kind of the risks.

The Need To Hedge The Portfolio

If Harish has invested his money in the market and for some reason or the other, the market is expected to go down, then there can be two possible scenarios that can be done:

- First is that if Harish is 100% sure that the market would go down, then he can take out his money (sell his shares) and book the profit and be

- Since there is a negligible chance that the above condition can be true, there is always uncertainty as to how the markets will perform; the better way to protect his savings is to hedge his portfolio.

Portfolio hedging in very simple terms is to mitigate the risk of market downturns. A hedge is an investment intended to move in the opposite direction of an asset in the portfolio that is considered to be at risk.

Hence, it becomes very crucial for Harish to hedge his portfolio for unexpected market swings.

How To Hedge Against Unsystematic Risks?

As mentioned earlier, unsystematic risks are the risks that are associated with a company or an industry. Hence, this can easily be mitigated through diversifying a portfolio.

Harish while making his portfolio can choose all the companies within a single industry. Let us say Harish chooses to invest in Infosys, TCS, Wipro, Mahindra Tech, and LnT Mind Tree. All of these are companies from the Tech industry. Hence, if something negative happens in the tech industry, then the portfolio of Harish incurs huge losses.

However, if Harish invests in companies from Healthcare and Consumer staples, which are negatively correlated with the tech industry (which means that when the tech industry goes down, healthcare and consumer staples go up), upward movement in these industries would mitigate then his losses from the tech industry.

Hence, unsystematic risk decreases when the portfolio becomes more diversified.

In the diagram shown above, it can be easily seen that as the number of stocks increases in the portfolio, the total risk of the portfolio decreases because the unsystematic risk reduces.

How To Hedge Against Systematic Risks?

In the above diagram, it can be seen that as the number of stocks increases or as we diversify the portfolio, the systematic risk remains the same. The systematic risk is not associated with any company or industry and hence it can be reduced by diversification. This is the residual risk.

To hedge against this risk, we use different derivative products such as:

- Futures: A futures contract is an agreement between two parties in which the parties can buy or sell the underlying asset (such as stocks, commodities, index) at a pre-determined price and pre-determined time

- Options: An option is a contract in which the buyer of the option has the right but not an obligation to buy or sell the underlying asset (such as stocks, commodities, index) at a pre-determined price and time

A few derivatives terminology:

Long Position: It is a position in which one would expect the price to go up in the future

Short Position: It is a position in which one would expect the price to go down in the future.

Call Option: The call option gives the right but not an obligation to buy the underlying asset at a pre-determined fixed price in the future. (European Option)

Put Option: The put option gives the right but not an obligation to sell the underlying asset at a pre-determined fixed price in the future. (European Option)

In this particular article, we will discuss hedging the portfolio using futures. Future contracts are traded on the exchange. A future contract can be explained using a simple example:

There is a piece of land. If I feel that the price of the land is going to rise, I will go ‘Long’ on the trade. If the current price of the land is Rs. 1 crore, I will ask the seller to fix the price of the land at Rs 1.2 crore but I will pay the price after 3 months. After 3 months, if the price of land is greater than 1.2 crores, I can sell the land to some other buyer booking a profit but if the price after 3 months is less than 1.2 crores, I will incur a loss. This is a forward contract.

A future contract is a standardized forward contract in an intermediate body, like an exchange, where the prices and the time durations are fixed by the exchange. In a forward contract, there is also a risk of default. After 3 months, I may not oblige to the contract and not give the Rs. 1.2 crores, if the price has fallen significantly. Exchange takes care of that too. It charges upfront margin money, which will be a percentage of the total contract (1.2 crores in this example) and it would deduct/add the amount based on what has happened after 3 months. This margin money is refundable.

Every future contact has to be squared off. For example, if we have gone long on the trade (i.e. bought the contract), then after the specified amount of time, I will have to sell the same number of contracts to square it off or to close the contract.

Now, back to Harish. If Harish expects the market to fall, he can take a short position on the portfolio using the futures. He will make money using the futures as he has taken a position expecting the market to fall. The loss in the portfolio would be offset by the gain in the futures contract. If the loss is completely offset by the gain in the future, we call it a perfect hedge.

In India, people generally trade in futures in NSE because of the higher liquidity than BSE. Hence, there could be 2 types of futures contracts:

- Single Stock Futures

- Index Futures

Hedging Using Single Stock Futures

Harish has five stocks in this portfolio. Let us assume that Reliance is one of them. We know the following information about Reliance {Assumptions}:

Spot Price (Current Market Price) – Rs. 2245

Price of one futures contract (3 months future) in NSE – Rs. 2090 {this means that Harish can buy 1 future contract right now for Rs. 2090}

Number of shares in 1 lot size of the contract – 700

Amount invested in Reliance – Rs. 7,80,00,000 {Assumption}

To hedge against the downfall in the market, Harish takes a ‘Short’ position. To calculate the amount of money to be hedged, we need to find the number of contracts Harish has to buy.

Value of 1 Contract = (Future price of the index) * (Lot Size)

Number of Contracts Shorted = [(Value of the Portfolio) / (Value of 1 Contract)] Total Hedge Amount = (Number of Contracts Shorted) * (Value of 1 Contract)

Hence, Harish needs to short 54 contracts of Reliance shares to hedge his investment in Reliance.

Now, after 3 months, the actual price of Reliance shares is Rs. 2070. Hence, the stock came down by around 7.8%. The value invested in Reliance has come down to Rs. 7,19,19,821.83.

There is a loss of Rs. 60,80,178.17 in the portfolio.

But, since we have shorted the Reliance share, there would be some gain from the squaring off the futures contract.

Selling Future Contract Value = Total Hedge Amount = (Number of Contracts Shorted) * (Value of 1 Contract)

Buying Future Contract (Squaring off Position) = (Number of Contracts Shorted) * (Spot Value of Index / Stocks after 3 months) * (Lot Size of each stock / Index)

Hence, by shorting the Reliance futures, Harish gained Rs. 7,56,000. The loss in the Reliance part was Rs. 60,80,178.17 but because of the futures, the loss was restrained to Rs. 53,24,178.17

This was hedging by single stock futures.

Hedging Using Index Futures

In the previous case, we have hedged only one share but what about four other stocks? We can hedge the full portfolio using any Index. We generally use Index because there are only 182 stocks in the NSE, which have their futures contract. If Harish has a stock, that is not on the list of these 182 stocks, he will hedge it using an Index. In our example, we will hedge it using the NIFTY 50 index.

We know the following information about NIFTY & the portfolio {Assumptions}:

Spot Price – Rs. 5395

Price of one futures contract (3 months future) of NIFTY 50 – Rs. 5269 {this means that Harish can buy 1 future contract right now for Rs. 5269}

Number of shares in 1 lot size of the contract – 50

Amount invested in Reliance – Rs. 3,00,00,00,000.00 {Assumption} Beta – 1.25 {this is the volatility of the portfolio with NIFTY 50}

We will follow a similar procedure as done earlier. However, there is a small change in one of the formulas.

Value of 1 Contract = (Future price of the index) * (Lot Size)

Number of Contracts Shorted = [(Beta * Value of the Portfolio) / (Value of 1 Contract)] Total Hedge Amount = (Number of Contracts Shorted) * (Value of 1 Contract)

Therefore, to hedge the full value of the portfolio, 14234 contracts have to be shorted. Now, if the Portfolio moves down by 6.75% the value of the portfolio decreases to Rs. 2,79,77,54,897.36. Hence, there is a total loss of Rs. 20,22,45,102.64.

The spot price of NIFTY 50 after 3 months is 5120. Hence, there would be a gain in squaring off the future contract. Similar formulas are used in the previous part.

The gain on the futures contract is Rs. 10,60,43,300.00.

With this gain in the future, the total loss in the portfolio is reduced to Rs. 9,62,01,802.64 compared to the loss of Rs. 20,22,45,102.64.

In both cases, the hedging is not perfect because there is an overall loss. In a perfect hedge, the overall loss would be zero.

Note – In both above cases, the values of the portfolio and the individual stock have been taken as large values to accentuate the difference between a hedged and an unhedged portfolio.

Conclusion

In conclusion, to make a great portfolio, one needs to consider asset and capital allocation. The risk-return profile is very important to gauge a portfolio. Risks are omnipresent and it is not possible to predict the market, hence we can only mitigate the risk. Unsystematic risk can be mitigated by diversifying the portfolio while systematic risk can mitigated using derivative products such as futures and options.

In addition, an important point to note here is that futures might prevent losses in the portfolio; it could also limit profit in case the portfolio moves up. Hence, derivate products like futures and options must be used very carefully and with utmost caution. Futures in this sense can be termed a “Double-Edged Sword”.

{kind=link}